Page – AZ (April 14, 2026) The City of Page has released its latest sales tax reports, and while the numbers may look uneven at first glance, the story behind them is far more interesting and far more reassuring.

Through most of the fall, the pattern was steady. Growth slowed from the rapid climb of the past few years, but it did not disappear. November remained strong, and December came in at $1,328,116 compared to $1,302,067 the year prior, an increase of about $26,000 or 2%. That is modest growth and does not outpace inflation, but it continues a multi year trend of increases.

The first real signal that things were shifting came earlier. October marked the first year over year decline in several years. It was not dramatic, but it was a flashing warning light that the pace of growth was beginning to normalize.

Then came January.

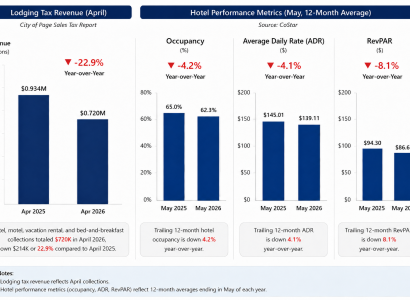

On paper, January stands out. Sales tax collections declined from $1,088,772 in January 2025 to $908,522 in January 2026, a drop of roughly $180,000 or 16.6%. Hotel and motel tax collections followed a similar pattern, falling from $373,560 to $232,118, a decrease of about 39%. That is a large gap and it should not be ignored.

But it also should not be misunderstood.

January 2025 appears to have been an unusually strong month not just locally, but across the State of Arizona. That created a high benchmark. When you compare this January to that kind of peak, the drop looks sharper than it really is in practical terms.

Even with that decline, collections remain well above what the city was seeing in fiscal years 2023 and 2024. And importantly, year to date city tax collections are still running about 11% ahead of where they were at this same point last year. That tells us the broader trajectory remains positive.

So what actually happened in January?

City tax data shows a sharp drop in total lodging revenue compared to a very strong prior year. At the same time, industry datasets show a more moderate picture within specific segments.

Data from CoStar Group, which tracks a sample of traditional hotel properties, indicates that hotel performance in January was comparatively stable, with occupancy largely flat year over year and average daily rate higher than the prior year. Because CoStar reflects a defined set of properties, it represents hotel performance rather than the full lodging market.

In contrast, data from AirDNA, which models short term rental activity, shows occupancy down about 5% in January compared to last year. While this data is based on estimates and does not capture every property, it suggests that some of the January softness may have been more pronounced in the short term rental segment.

Taken together, these datasets indicate that January was likely driven by a combination of a high prior year comparison, seasonal shifts in travel patterns, and differences across lodging segments, rather than a broad collapse in demand.

Looking beyond January, broader trend data provides additional context. According to data provided by CoStar Group, Page’s trailing 12 month RevPAR is down about 5.7%, with occupancy down roughly 1.8%. Because this is a rolling twelve month measure, it reflects overall market conditions and smooths out short term fluctuations like those seen in January.

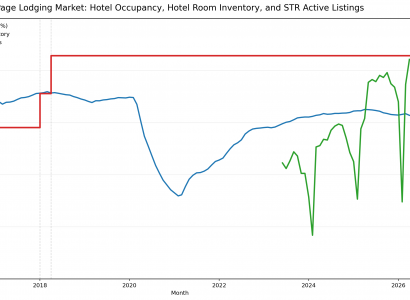

Nearby destinations tell a similar story. Moab and Kanab are only slightly down. Flagstaff and Williams have seen more noticeable declines. Higher end markets like Sedona and Scottsdale are holding up a bit better, but even there, the rapid growth of recent years has slowed.

Zoom out further, and the same pattern appears across the country. Las Vegas has seen a meaningful pullback. Washington is also down. Meanwhile, New York and Miami continue to show growth. Some markets are up. Some are down. The common thread is that the surge of the past few years has given way to a more balanced environment.

And then there is February.

More recent data points suggest improving conditions in Page. According to AirDNA, short term rental occupancy in February improved significantly, narrowing to within about 2% of prior year levels. Separately, monthly hotel data for Page indicates stronger performance in February compared to January, with higher occupancy, continued strength in pricing, and an increase in RevPAR of roughly $6 year over year.

That improvement matters. It suggests that January was not the start of a downward trend, but rather a short term adjustment following an unusually strong prior year.

For local businesses, the takeaway is straightforward. The market is not declining. It is settling into a more sustainable rhythm after a period of unusually fast growth. Demand is still there. Visitors are still coming. The difference is that the pace is becoming more consistent and more predictable.

Page remains a destination people plan for, travel to, and remember. That has not changed.

If anything, the latest data shows a market that is finding its footing at a higher level than before. And for a tourism driven community, that is a strong place to be.

NOTE: CoStar and AirDNA data reflects aggregated performance of participating properties and industry estimates, and is provided for general market context.